著者

Daniel Taylor

マン・グループ システマティック部門副CIO 兼 マン・ニューメリック CIO

2026年下半期に向け、われわれは定量運用マネジャーとして、AIがテクノロジー・セクター全体にもたらしている格差を注視していく方針です。

主要点

・AIに対する熱狂は、半導体セクターの株価急騰とソフトウェア・セクターの苦境という極端な分断をもたらしています。われわれはAI投資の収益化の道筋が見えてくるまで、このような格差は継続するとみています。

・足元ではハイパースケーラー(クラウドサービスを大規模に構築・運用する企業)の営業キャッシュフローの9割超をAI設備投資が占めている中で、フリーキャッシュフローは大きな転換点を迎えています。投資家は投資ペースの適正化を求めていますが、それが実現すれば半導体需要に対する逆風となるものと思われます。

・足元の半導体セクターのバリュエーションは、一切の悪材料が許されない「完璧」を前提とした価格設定となっています。今後予定されているAI企業のIPO(新規株式公開)は、現在のAI投資ブームが今後も続くのかを見極めるうえで、重要な試金石となるものと思われます。

***

グローバル株式市場は、2026年上半期のイラン戦争や金利上昇といった悪材料をものともせず、史上最高値あるいはそれに近い水準を維持しています。このような強気な姿勢は、AIを巡る楽観的な見方が原動力となっています。しかしながら、AIに対する熱狂は、半導体セクターの株価急騰とソフトウェア・セクターの苦境という極端な分断を引き起こしています。われわれは定量運用マネジャーとして、下半期にこの状況がどう推移していくのかを注意深く見守っていく方針です。

AIに対する熱狂的な投資意欲を背景に、半導体関連銘柄は年初来のS&P500指数の上昇分の約3分の2、韓国KOSPI指数の80%という大幅上昇の大部分を担ってきました。その対極で起きているのが「SaaSアポカリプス(SaaS銘柄の崩壊)」と呼ばれる現象で、SaaS(Software-as-a-Service)銘柄の広範な売りが、Microsoftをはじめとするソフトウェア・セクター全体の足を引っ張っています。さらに、ハイパースケーラーがこれまで創出してきたフリーキャッシュフローの大部分が、AIへの巨額投資によって消失している事態となっています。

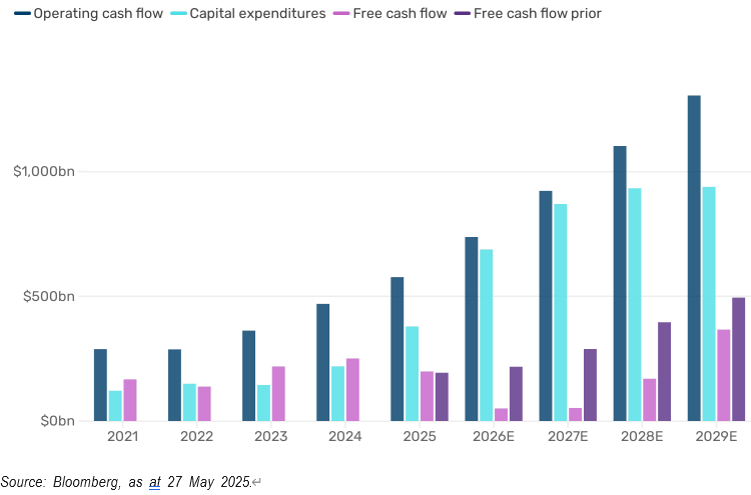

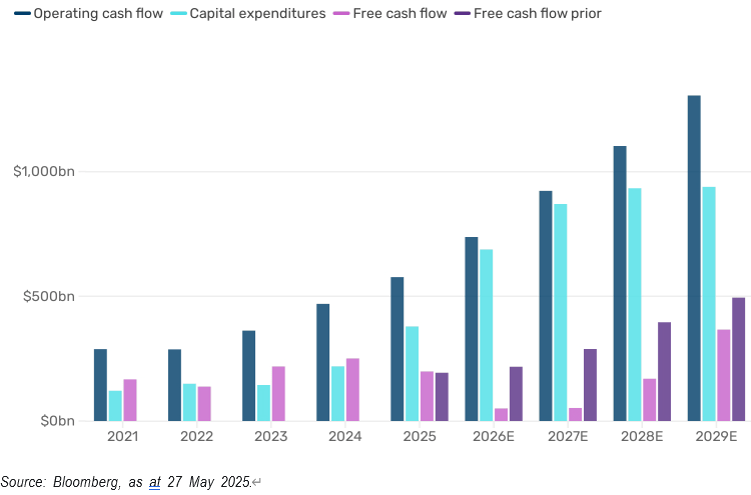

2025年9月発行のレポート「Musical Chairs AI Edition – Listen Carefully!」でわれわれは、ハイパースケーラーの設備投資の増加が営業キャッシュフローの伸びを相殺することでフリーキャッシュフロー総額は2025年と2026年に約2,000億米ドルまで落ち込むものの、2027年以降は過去最高を更新して急増すると予想していました。

しかしながら、直近2四半期の決算に基づくと、ハイパースケーラーの営業キャッシュフローの90%以上は依然設備投資に向かう見通しとなっており、フリーキャッシュフローが再び過去最高水準を更新するのは2029年以降となる可能性が高くなっています。30年以上にわたりプラスのフリーキャッシュフローを維持してきたOracleでさえ、今では5年連続でマイナスに陥ると予想されています。

図表1:ハイパースケーラー(Microsoft、Amazon、Meta、Google、Oracle)のキャッシュフローと設備投資(単位:10億米ドル)の推移 ☑拡大画像

☑拡大画像

S&P 500指数およびMSCIワールド指数において、Microsoft、Amazon、Meta、Google、Oracleの5社にNVIDIAを加えた6社が占める累積ウェイトは、それぞれ26.3%と18.6%であり、おおむね横ばいで推移しています。しかしながら、このグループ内では大きな格差が生じています。最大の恩恵を受けているのはNVIDIAであり、AIの収益化や独自設計のAI半導体事業に対する期待感から、Alphabet(Google)がその次に続いています。その一方で、Microsoft、Meta、Oracleは、設備投資の増加や固有の懸念材料によって苦戦を強いられています。ハイパースケーラーの投資機会については後述しますが、まずはこのセクターにおける最大の勝者と敗者を比較し、負の側面がもたらすリスクを確認したいと思います。

半導体セクター 対 ソフトウェア・セクター

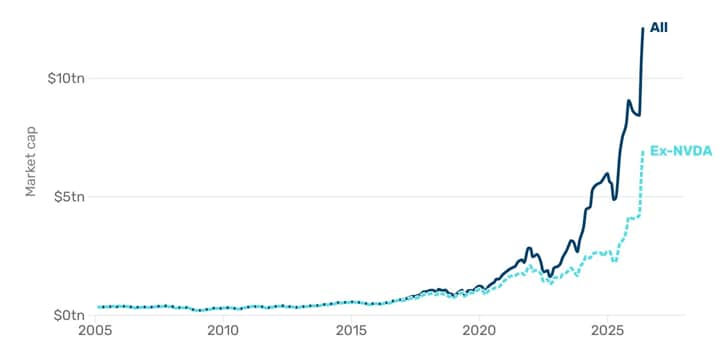

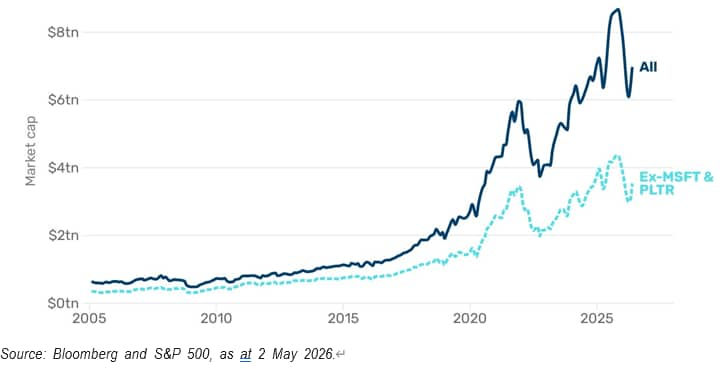

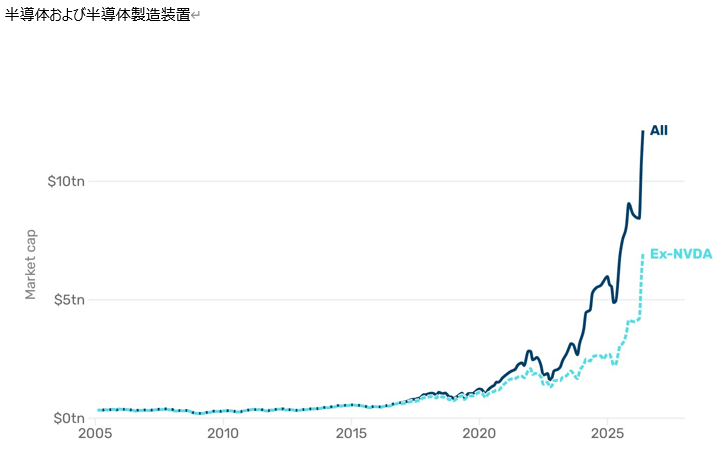

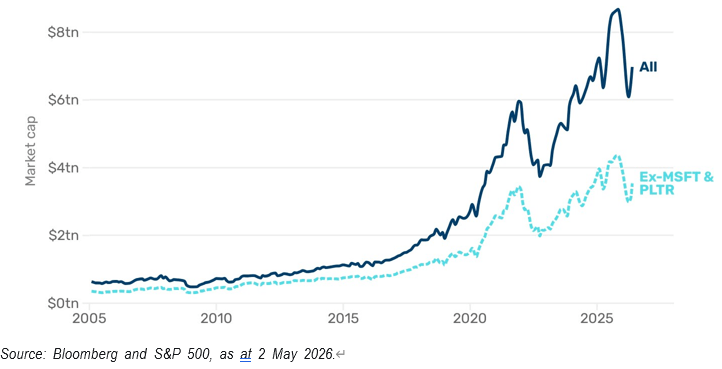

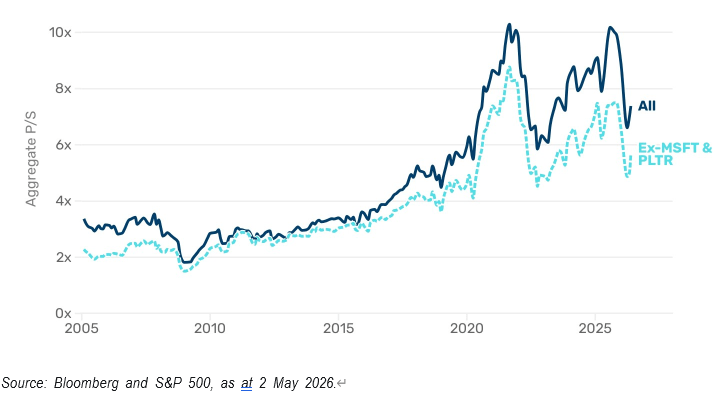

図表2:AIブームがテクノロジー・セクターを二分している

【半導体および半導体製造装置】

☑拡大画像

☑拡大画像

【ソフトウェアおよびサービス】

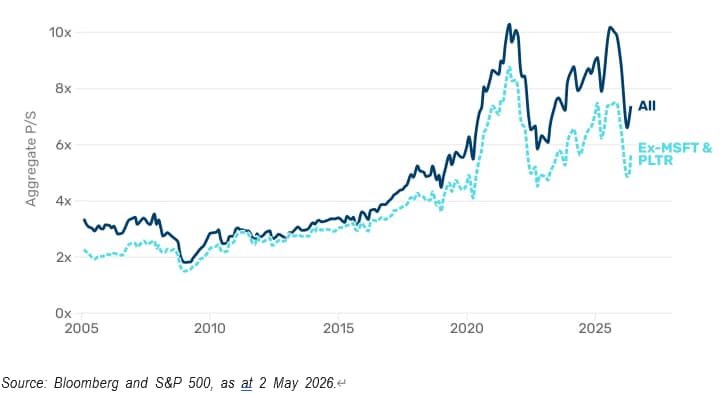

バリュエーションの観点から見ると、ソフトウェア・セクターへの投資を正当化することは容易ではありません。セクター全体の株価売上高倍率(PSR)は約7倍で、MicrosoftとPalantirを除くと6倍未満となっています。これは過去5年間の水準を下回っているものの、より長期的な平均水準と比較すると、依然として大幅に高い水準にあります。われわれは、ソフトウェア業界が消滅するなどとは考えておらず、足元においても有望な投資機会は存在していると見ています。しかしながら、成長回復の兆候が確認されるまでは、現在進行中のバリュエーション低下がさらに続く可能性が高いと考えています。

図表3:ソフトウェア・サービス・セクターのバリュエーションは2021年のピークから低下しているものの、依然として長期的な平均水準を大きく上回っている

☑拡大画像

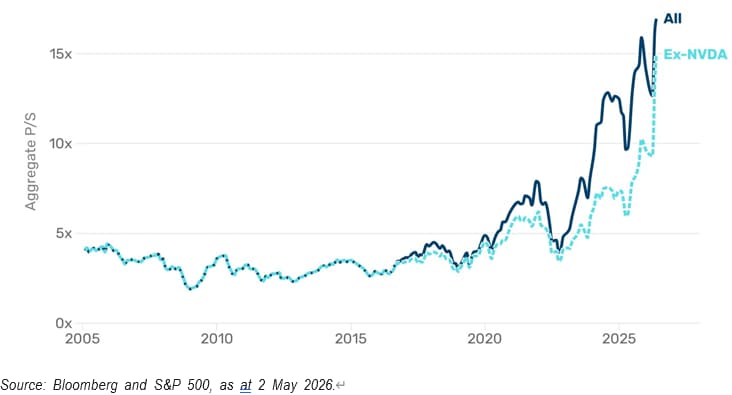

一方で、半導体セクターのバリュエーションの評価はより明確ですが、それは決して好ましい意味合いにおいてではありません。NVIDIAを含めるか除外するかにかかわらず、半導体セクター全体の株価売上高倍率(PSR)は、2005年から2020年までの間は2倍から4倍の範囲で推移していました。2020年から2021年にかけての強気相場で急上昇した後、2022年後半には一時的に4倍の水準まで戻りました。しかしそれ以降は16倍超(NVIDIAを除いても14倍超)へと急激に上昇しています。明らかに、これは半導体に対する前例のない成長期待を織り込んだ価格設定です。しかしそれは、AIインフラの構築ペースが減速した際、悪材料を吸収する余地がほとんど、あるいは全くないことを意味しているように思われます。もちろん、そのような減速がいつ起きるかは誰にも分からず、仮に2030年以降になるのであれば、現在のバリュエーションは極めて妥当なものと言えるかもしれません。それでもやはり、半導体関連銘柄は「完璧なシナリオ」を完全に織り込んだ水準(priced for perfection)にあるような危うさを感じさせます。企業業績がこのバリュエーションに見合うレベルまで成長するには、相応の時間が必要になるものと思われます。

図表4:足元の半導体セクターのバリュエーションは過去20年の平均から逸脱し、「完璧なシナリオ」を織り込んだ価格設定となっている

☑拡大画像

最終カウントダウン?

ここで、先ほど後述すると述べたハイパースケーラーの投資機会に話を戻します。留意すべきは、ハイパースケーラーの投資妙味が改善するということは、半導体セクターの最大のリスクに直結するという構図です。過去15年間の大部分において、Microsoft、Alphabet、Metaといった企業は、並外れたキャッシュフローを創出してきました。このような企業は、資産の軽い(アセットライトな)ビジネスモデルを持ち、自己資金で成長を賄うことができ、株主に対して極めて高いリターンをもたらしてきました。ここ数年、AI関連の設備投資は急増しており、市場予想を上回り続けていますが、われわれは極めて重要な転換点に近づいている可能性があります。

それは、仮にAI関連の設備投資が現在の予想を上回った場合、ハイパースケーラーのフリーキャッシュフローが大幅なマイナスに転落しかねないというものです。われわれは、現時点ではそのような結果に陥る可能性は低いとみています。一例としてOracleの株価は、同社の株式希薄化を伴う資金調達の必要性が織り込まれたことで、高値から大きく下落した水準にあります。

また、今後予想されるSpaceX、OpenAI、さらにはAnthropicのIPO(新規株式公開)を通じて、AI関連支出の持続可能性について、より多くの洞察を得ることができる可能性があります。しかしながら、世界的な金利が高止まりしている中で、資本コストの上昇は無視できない現実問題となっているため、われわれは投資家はハイパースケーラーによる投資抑制を歓迎するだろうと考えています。

しかしながら、その投資抑制は、半導体セクターの大幅な価格調整をもたらす可能性があります。別の言い方をすれば、われわれは、AIブームの「第2章」がどのような展開を見せるかが明らかになるまで、足元の極端な二極化は継続する可能性が高いと考えています。

For more information on some of the key terms mentioned in this article, our Glossary may be found here: man.com/glossary

Important Information

This information is communicated and/or distributed by the relevant Man entity identified below (collectively the "Company") subject to the following conditions and restriction in their respective jurisdictions.

Opinions expressed are those of the author and may not be shared by all personnel of Man Group plc (‘Man’). These opinions are subject to change without notice, are for information purposes only and do not constitute an offer or invitation to make an investment in any financial instrument or in any product to which the Company and/or its affiliates provides investment advisory or any other financial services. Any organisations, financial instrument or products described in this material are mentioned for reference purposes only which should not be considered a recommendation for their purchase or sale. Neither the Company nor the authors shall be liable to any person for any action taken on the basis of the information provided. Some statements contained in this material concerning goals, strategies, outlook or other non-historical matters may be forward-looking statements and are based on current indicators and expectations. These forward-looking statements speak only as of the date on which they are made, and the Company undertakes no obligation to update or revise any forward-looking statements. These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those contained in the statements. The Company and/or its affiliates may or may not have a position in any financial instrument mentioned and may or may not be actively trading in any such securities. Unless stated otherwise all information is provided by the Company. Past performance is not indicative of future results.

Unless stated otherwise this information is communicated by the relevant entity listed below.

Australia: To the extent this material is distributed in Australia it is communicated by Man Investments Australia Limited ABN 47 002 747 480 AFSL 240581, which is regulated by the Australian Securities & Investments Commission ('ASIC'). This information has been prepared without taking into account anyone’s objectives, financial situation or needs.

Austria/Germany/Liechtenstein: To the extent this material is distributed in Austria, Germany and/or Liechtenstein it is communicated by Man (Europe) AG, which is authorised and regulated by the Liechtenstein Financial Market Authority (FMA). Man (Europe) AG is registered in the Principality of Liechtenstein no. FL-0002.420.371-2. Man (Europe) AG is an associated participant in the investor compensation scheme, which is operated by the Deposit Guarantee and Investor Compensation Foundation PCC (FL-0002.039.614-1) and corresponds with EU law. Further information is available on the Foundation's website under www.eas-liechtenstein.li.

European Economic Area: Unless indicated otherwise this material is communicated in the European Economic Area by Man Asset Management (Ireland) Limited (‘MAMIL’) which is registered in Ireland under company number 250493 and has its registered office at 70 Sir John Rogerson's Quay, Grand Canal Dock, Dublin 2, Ireland. MAMIL is authorised and regulated by the Central Bank of Ireland under number C22513.

Hong Kong SAR: To the extent this material is distributed in Hong Kong SAR, this material is communicated by Man Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission in Hong Kong.

Japan: To the extent this material is distributed in Japan it is communicated by Man Group Japan Limited, Financial Instruments Business Operator, Director of Kanto Local Finance Bureau (Financial instruments firms) No. 624 for the purpose of providing information on investment strategies, investment services, etc. provided by Man Group, and is not a disclosure document based on laws and regulations. This material can only be communicated only to professional investors (i.e. specific investors or institutional investors as defined under Financial Instruments Exchange Law) who may have sufficient knowledge and experience of related risks.

Switzerland: To the extent this material is made available in Switzerland the communicating entity is Man Investments AG, Huobstrasse 3, 8808 Pfäffikon SZ, Switzerland, which is regulated by the Swiss Financial Market Supervisory Authority (‘FINMA’).

United Kingdom: Unless indicated otherwise this material is communicated in the United Kingdom by Man Solutions Limited ('MSL') which is a private limited company registered in England and Wales under number 3385362. MSL is authorised and regulated by the UK Financial Conduct Authority (the 'FCA') under number 185637 and has its registered office at Riverbank House, 2 Swan Lane, London, EC4R 3AD, United Kingdom.

United States: To the extent this material is distributed in the United States, it is communicated and distributed by Man Investments, Inc. (‘Man Investments’). Man Investments is registered as a broker-dealer with the SEC and is a member of the Financial Industry Regulatory Authority (‘FINRA’). Man Investments is also a member of the Securities Investor Protection Corporation (‘SIPC’). Man Investments is a wholly owned subsidiary of Man Group plc. The registration and memberships described above in no way imply a certain level of skill or expertise or that the SEC, FINRA or the SIPC have endorsed Man Investments. Man Investments Inc, 1345 Avenue of the Americas, 21st Floor, New York, NY 10105.

This material is proprietary information and may not be reproduced or otherwise disseminated in whole or in part without prior written consent. Any data services and information available from public sources used in the creation of this material are believed to be reliable. However accuracy is not warranted or guaranteed. © Man 2026

MKT019834/NS/GL/W

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}