著者

Daniel Taylor

システマティック部門共同ヘッド、マン・ニューメリックCIO

2026年にクオンツ・マネジャーであるわれわれが注目している主要指標

われわれクオンツ・マネジャーは、主観的判断に基づく予測を重視していません。その代わり、われわれは定量化が可能であり、かつ過去のデータと比較可能な指標を用いて、将来の見通しを組み立てています。本レポートでは、われわれがクオンツ・マネジャーとして今後1年を通じて注視する指標について説明いたします。

1:絶対ベースのバリュエーション

株式市場がじりじりと上昇を続ける中、多くの投資家が絶対ベースでの個別銘柄のバリュエーション水準に懸念を抱いています。われわれは、市場の投資タイミングを計ることは(少なくともバリュエーションに関して)極めて困難であるため、銘柄間の相対的なバリュエーション水準に着目することが重要であると考えています。とはいうものの、足元では時価総額が大きい一部の銘柄の株価が、絶対ベースで極めて割高になっている可能性があることも事実です。

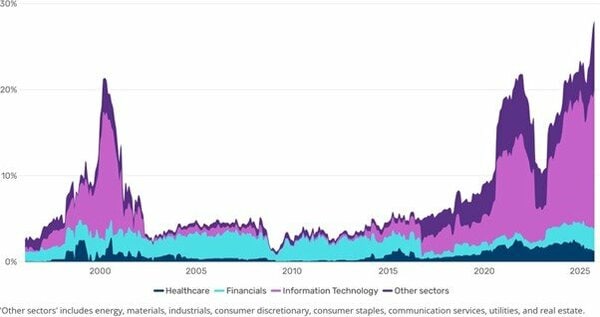

EV/売上高倍率は、企業の企業価値を年間売上高と対比させる指標です。この指標は、その株式が割安か割高かを評価するもので、一般的に倍率が低いほど割安な銘柄であることを示唆します。足元では、MSCIワールド指数の構成ウェイトの25%以上でEV/売上高倍率が10倍超となっており、高水準であったドットコムバブル期やコロナ禍後の局面を上回っています。われわれはこのような状況はいずれ正常化し始めると考えていますが、焦点となるのは、これらの特定の銘柄(その大半は米国のハイテク株)の株価の上昇を正当化できるほどのペースで、売上が成長できるかどうかという点です。

図表1:EV/売上高倍率が10倍超(上段)および20倍超(下段)のセクターが、MSCIワールド指数に占めるウェイトの合計

Source: Man Numeric.

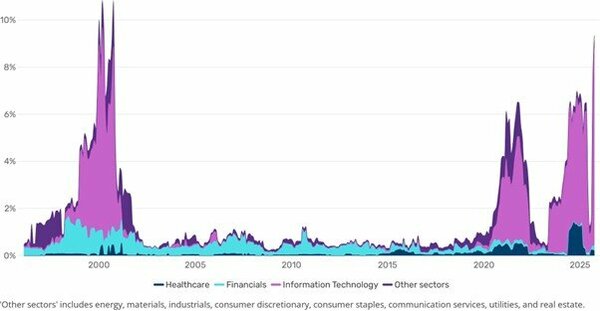

2:予想益利回り(earnings-to-price (E/P) )

絶対ベースのバリュエーション以外の他の指標は、グローバル株式市場がそれほど異常な状態にあることを示唆してはいません。図表2は、「バリュエーション・ストレッチ」※1を評価する上で、われわれが重視している指標を示しています。この指標は、様々な地域の株式市場において、セクター内での予想益利回りのばらつき程度に焦点を当てたもので、各銘柄の今後12ヶ月の予想一株当たり利益(EPS)をセクター相対で比較しそのばらつき度合いを見ることで、フォワードルッキングな視点に基づく相対的な株価の割安度比較が可能となります。

縦軸は、各地域のこの指標のZスコア※2の時系列推移を示しています。相対ベースで見たバリューの観点からの投資機会は、2000年代初頭、2009年、および2020年から2022年にかけて大きく拡大していたものの、足元では米国大型株と日本株という2つの例外を除けば、概ね銘柄間の予想益利回りで見たバリュエーションのばらつきは、平均的な水準にあります。米国大型株では、バリュエーション・ストレッチは約+1シグマ※3に達しており、通常よりもバリューの観点からの投資機会が広がっていること(=銘柄間のバリュエーションの格差が大きい)を示唆しています。対照的に、日本株は約-0.8シグマ※4となっており、バリューの観点からの投資機会が小さいことを示唆しています。これに基づくと、他の条件が同じであり、株価がバリュエーションを反映した適正な水準へと向かえば、2026年の割安度に着目した株式投資は標準的なパフォーマンスになると予想されます。地域別では、日本株ではパフォーマンスがやや抑制され、米国大型株ではより高い水準となる可能性があります。

※1=株価のファンダメンタルズ価値からの乖離状況、※2=訳注:標準偏差を用いた乖離度、※3=正規分布曲線における平均値から右側に1標準偏差、※4=左側に1標準偏差

図表2:予想益利回り(E/P)のばらつき度合の推移

Source: Man Numeric.

3. マクロ環境:過去と現在との比較

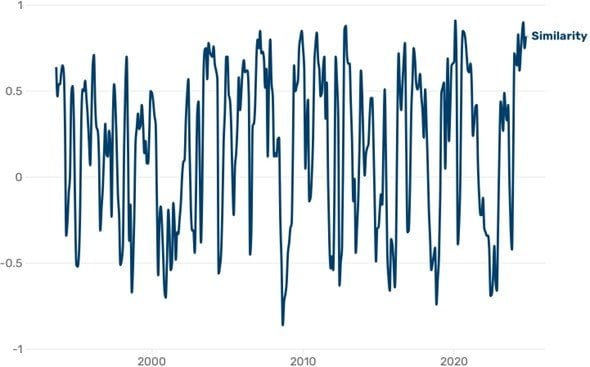

われわれが注力しているもう一つの分野は、過去との比較で現在のマクロ環境を特定し、同様の局面においてスタイルやセクターがどのようなパフォーマンスを示したかを分析することです。図表3は、1994年から2025年までの期間で見た場合の現在(1)のマクロ環境との類似性を示しています。ここから足元の環境は、1年前や2020年※、2010年から2013年の一定期間、そして2003年と非常によく似ていることが分かります。これらの期間に共通する要因としては、堅調な株式市場、イールドカーブのスティープ化、そして貴金属の好調なパフォーマンス、などが挙げられます。現在われわれのモデルは、スタイル別ではモメンタム・ファクターを最も選好しており、次いでクオリティ、収益性、グロース・ファクターとなっています。セクターではエネルギーや一部の素材セクターを選好している一方で、金や貴金属については不振となると予想されています。この点は明らかにここ最近の貴金属の価格動向とは大きく異なっているため、2026年を通じて価格が実際にどのように推移するかは非常に興味深い点であると思われます。

※パンデミックによる暴落局面を除く

図表3:足元のマクロ環境(過去との類似性)

Source: Man Numeric.

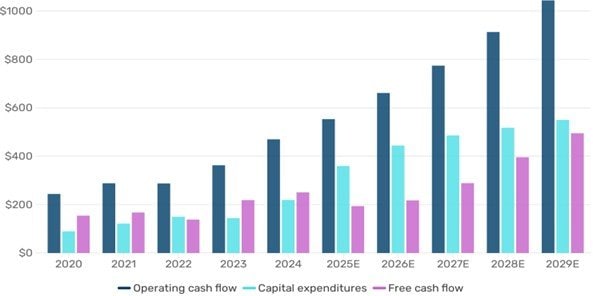

4. AI関連の設備投資

最後に、2026年の株式投資家にとって重要な点は、足元のAI関連の設備投資のペースがどの程度持続可能かということです。過去数回の決算シーズンにおいて、われわれはクラウドサービスを大規模に構築・運用するハイパースケーラーの今後の設備投資計画に注目してきました。設備投資のペースに何らかの変化があれば、関連企業のみならず、株式市場全体や世界経済にも重大な影響を与える可能性があります。

NVIDIA、Microsoft、Amazon、Meta、Alphabet、Oracleは合計で、S&P 500の26.5%、MSCIワールドの18.5%を占めています(2)。この6企業のうちのNVIDIA以外の5社※の設備投資額は、過去2年間で大幅に増加しました。われわれはこの増加傾向が続くと予想しており、その結果2025年と2026年のフリーキャッシュフローは、2024年の水準を下回る可能性があります。

※従来のハイパースケーラー4社と新規参入者であるOracle

図表4:Microsoft、Amazon、Meta、Google、Oracleのキャッシュフローと設備投資の推移と今後の予測(単位:10億米ドル)

Source: Bloomberg.

今後の見通し

クオンツ・マネジャーであるわれわれは予測は行いません。しかしながら、われわれのモデルに基づけば、足元のバリュエーションは絶対ベースで割高であるように見えるものの、バリュエーション・ストレッチ※1や過去のマクロ環境との類似性の観点から見た場合には、2026年を通して米国大型株は底堅く推移する可能性があります。この点は、AI関連の設備投資が増加し、短中期的な投資利益率(ROI)が不透明である(成長加速か、コスト効率化か、あるいは何の成果も生まないか)という状況下であっても揺るがないものと思われます。

株式以外の他の資産クラスの見通しは、米国債の安全資産としての特性に部分的に依存するものの、資産クラス固有の要因にも影響を受ける可能性があります。オックスフォード・マン定量的ファイナンス研究所(Oxford-Man Institute of Quantitative Finance)のパートナーの一人であるハーベイ教授は、金の実質価格は超長期的には一定である(インフレ調整後では価値が変わらない)、という仮説を立てています。そう考えると、金価格が平均値近くまで回帰するというわれわれのモデルの予測は、一見するほど驚くべきものではないかもしれません。いずれにせよ、われわれは環境の変化を示す小さな異変や兆候を見逃さぬよう、独自に開発したマクロスコープモデル※2を注視し続ける方針です。

※1=益利回りの上位銘柄群と下位銘柄群の差分、※2=Macroscope:足元の経済金融環境に類似した過去局面で有効であったファクターに追随して個別銘柄を選択するモデル

(1)As of 9 October 2025、(2)As of 9 October 2025

特段の記載がない限り、すべてのデータはブルームバーグに基づいています。

For more information on some of the key terms mentioned in this article, our Glossary may be found here: man.com/glossary

Important Information

This information is communicated and/or distributed by the relevant Man entity identified below (collectively the

"Company") subject to the following conditions and restriction in their respective jurisdictions.

Opinions expressed are those of the author and may not be shared by all personnel of Man Group plc (‘Man’). These opinions are subject to change without notice, are for information purposes only and do not constitute an offer or invitation to make an investment in any financial instrument or in any product to which the Company and/or its affiliates provides investment advisory or any other financial services. Any organisations, financial instrument or products described in this material are mentioned for reference purposes only which should not be considered a recommendation for their purchase or sale. Neither the Company nor the authors shall be liable to any person for any action taken on the basis of the information provided. Some statements contained in this material concerning goals, strategies, outlook or other non-historical matters may be forward-looking statements and are based on current indicators and expectations. These forward-looking statements speak only as of the date on which they are made, and the Company undertakes no obligation to update or revise any forward-looking statements. These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those contained in the statements. The Company and/or its affiliates may or may not have a position in any financial instrument mentioned and may or may not be actively trading in any such securities. Unless stated otherwise all information is provided by the Company. Past performance is not indicative of future results.

Se non diversamente indicato, queste informazioni sono comunicate dall'ente di riferimento elencato di seguito.

Australia: To the extent this material is distributed in Australia it is communicated by Man Investments Australia Limited ABN 47 002 747 480 AFSL 240581, which is regulated by the Australian Securities & Investments Commission ('ASIC'). This information has been prepared without taking into account anyone’s objectives, financial situation or needs.

Austria/Germany/Liechtenstein: To the extent this material is distributed in Austria, Germany and/or Liechtenstein it is communicated by Man (Europe) AG, which is authorised and regulated by the Liechtenstein Financial Market Authority (FMA). Man (Europe) AG is registered in the Principality of Liechtenstein no. FL-0002.420.371-2. Man (Europe) AG is an associated participant in the investor compensation scheme, which is operated by the Deposit Guarantee and Investor Compensation Foundation PCC (FL-0002.039.614-1) and corresponds with EU law. Further information is available on the Foundation's website under www.eas-liechtenstein.li.

European Economic Area: Unless indicated otherwise this material is communicated in the European Economic Area by Man Asset Management (Ireland) Limited (‘MAMIL’) which is registered in Ireland under company number 250493 and has its registered office at 70 Sir John Rogerson's Quay, Grand Canal Dock, Dublin 2, Ireland. MAMIL is authorised and regulated by the Central Bank of Ireland under number C22513.

Hong Kong SAR: To the extent this material is distributed in Hong Kong SAR, this material is communicated by Man Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission in Hong Kong.

Japan: To the extent this material is distributed in Japan it is communicated by Man Group Japan Limited, Financial Instruments Business Operator, Director of Kanto Local Finance Bureau (Financial instruments firms) No. 624 for the purpose of providing information on investment strategies, investment services, etc. provided by Man Group, and is not a disclosure document based on laws and regulations. This material can only be communicated only to professional investors (i.e. specific investors or institutional investors as defined under Financial Instruments Exchange Law) who may have sufficient knowledge and experience of related risks.

Switzerland: To the extent this material is made available in Switzerland the communicating entity is Man Investments AG, Huobstrasse 3, 8808 Pfäffikon SZ, Switzerland, which is regulated by the Swiss Financial Market Supervisory Authority (‘FINMA’).

United Kingdom: Unless indicated otherwise this material is communicated in the United Kingdom by Man Solutions Limited ('MSL') which is a private limited company registered in England and Wales under number 3385362. MSL is authorised and regulated by the UK Financial Conduct Authority (the 'FCA') under number 185637 and has its registered office at Riverbank House, 2 Swan Lane, London, EC4R 3AD, United Kingdom.

United States: To the extent this material is distributed in the United States, it is communicated and distributed by Man Investments, Inc. (‘Man Investments’). Man Investments is registered as a broker-dealer with the SEC and is a member of the Financial Industry Regulatory Authority (‘FINRA’). Man Investments is also a member of the Securities Investor Protection Corporation (‘SIPC’). Man Investments is a wholly owned subsidiary of Man Group plc. The registration and memberships described above in no way imply a certain level of skill or expertise or that the SEC, FINRA or the SIPC have endorsed Man Investments. Man Investments Inc, 1345 Avenue of the Americas, 21st Floor, New York, NY 10105.

This material is proprietary information and may not be reproduced or otherwise disseminated in whole or in part without prior written consent. Any data services and information available from public sources used in the creation of this material are believed to be reliable. However accuracy is not warranted or guaranteed. © Man 2025